Most families who build extraordinary wealth focus on how to grow it. Fewer think carefully about what happens when the number of people drawing from it multiplies.

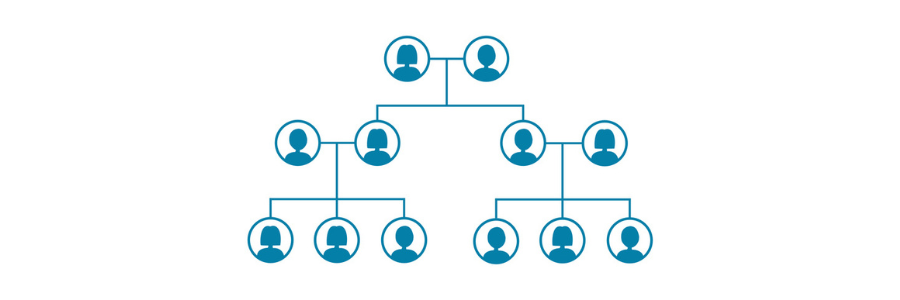

A $500 million fortune sounds inexhaustible. For a founding couple and their three children, it likely is true. But wealth is not static, and families do not stay small. By the third generation, that founding couple may have eight or twelve grandchildren, each with a spouse, a household, a lifestyle, and expectations shaped by the generation before them.

This is the arithmetic that most families underestimate: consumption does not just grow with inflation, it grows exponentially across generations just as the family itself does.

The Arithmetic of Family Growth

Consider a family with $500 million in investable assets. In the first generation, two principals draw on the portfolio. Their consumption, however generous, is contained. Perhaps they spend $2.5 million a year between them, a 0.5% consumption rate that is well within the annual return of a diversified, long-horizon portfolio.

By the second generation, those two principals have three adult children, each with a partner. That is eight adults, and four separate households, each with its own cost of living, property, travel, education expenses, and lifestyle expectations.

By the third generation, assume each of those three children has three children of their own. That is nine grandchildren, eventually nine more households, which totals thirteen households. With the increase in households and fifty years of inflation, annual family consumption can easily increase past $60 million.

You can follow the consumption trend as we enter the fourth and fifth generation. Hopefully, the pool of wealth has grown as quickly as the mouths it feeds.

A Rare Position, Easily Misunderstood

It is worth pausing to acknowledge how rarefied this position is. According to Knight Frank’s The Wealth Report 2025, the global population of individuals with a net worth of $100 million or more surpassed 100,000 for the first time in 2025. This number is such a small fraction it barely registers as a percentage of the world’s eight billion people. A family sitting at $500 million belongs to an even thinner slice. Altrata’s Billionaire Census 2025 counted just 3,508 billionaires globally, so there are somewhere between 3,500 and 100,000 families with $500 million in net worth.

That rarity can breed a false sense of permanence. When the number feels so large, it is easy to assume it will always be enough. But wealth at this scale carries a paradox: the lifestyle it enables is precisely what can erode it, especially when that lifestyle multiplies across a growing family.

Consumption Inflates Differently at the Top

The challenge deepens when you account for the cost of living at this level. Forbes’ Cost of Living Extremely Well Index, which tracks a basket of forty luxury goods and services (from private jets and motor yachts to concierge services and estate staff), rose 5.5% in 2025, exactly double the 2.7% increase in the Consumer Price Index.

This means that even if a family’s consumption habits remain constant in real terms, the dollar cost of those habits rises faster than the broader economy. A family spending $15 million a year is not spending $15 million in five years. At 5.5% annual luxury inflation, they are spending closer to $20 million, without changing a single thing about how they live.

When that escalation meets generational expansion, the compounding effect accelerates.

What the Research Shows

The widely cited statistic that 70% of wealthy families lose their wealth by the second generation, and 90% by the third, has been questioned in recent years. Wealth consultant James Grubman has argued that the research behind these figures is flawed or overstated, and that the statistic itself can become self-fulfilling when parents respond by shielding children from financial education rather than preparing them.

But the underlying dynamic is real. Families do not lose wealth primarily through poor investments or economic downturns. More often, the erosion is gradual: rising consumption, expanding family size, insufficient communication between generations, and a disconnect between lifestyle expectations and portfolio capacity.

The Family Office Cannot Plan What It Cannot See

Here is where the problem becomes structural. In many families, consumption is treated as a personal matter. This becomes a serious problem when each generation and each household manages its own spending without visibility into the whole.

But for the family office or wealth manager, consumption is not personal. It is a business and portfolio input.

Every dollar consumed is a dollar not compounding. Every increase in aggregate family spending changes the required return profile of the portfolio. It shifts asset allocation, alters liquidity needs, compresses time horizons, and reduces the capital available for illiquid, long-duration investments, which are often the very investments that generate the strongest returns over time.

When a family office does not have clear visibility into current and projected consumption across all branches of the family, it is making investment decisions with incomplete information. It may be underestimating liquidity needs. It may be over-allocating to illiquid vehicles. It may be assuming a longer time horizon than the family’s spending trajectory actually supports.

This is not a theoretical risk. It is an operational one.

What Families Can Do

The solution is not austerity. Ultra-high-net-worth families should live well if that is their decision. That is the freedom their wealth brings them. But living well and living without awareness are different things.

First, the family and its advisors should talk about consumption as a strategic topic. Early education on the responsibilities and expectations of wealth prepares the next generation. Additionally, open communication on the impacts of consumption, not only creates transparency between family members, but allows the family office to plan accordingly.

Every family has a number: the level of aggregate consumption at which the portfolio can no longer sustain itself across the next generation. Most families do not know what that number is. Their family office should know it and should inform the family.

Second, consumption should be visible. Every branch of the family should have a clear sense of what it can draw and what it does draw from the shared pool, and the family office should have the data it needs to model the full picture.

Third, consumption should be projected, not just tracked. Understanding what the family spends today matters less than understanding what it will spend in ten, twenty, or thirty years as the family grows. Those projections, including assumptions about new households, lifestyle inflation, and the cost of maintaining the family’s standard of living, should inform portfolio construction and asset allocation directly.

The families that endure across generations are rarely the ones who spend the least. They are the ones who understand the relationship between what they consume and what they invest.

Don’t shy away from discussions on consumption. Make it part of a regular check in with your family office. There are many dangers to a family’s wealth, but the exponentially growing draw on wealth from consumption as generations pass on is one that can be planned for.

——

For more content, check out Wingspan Insights